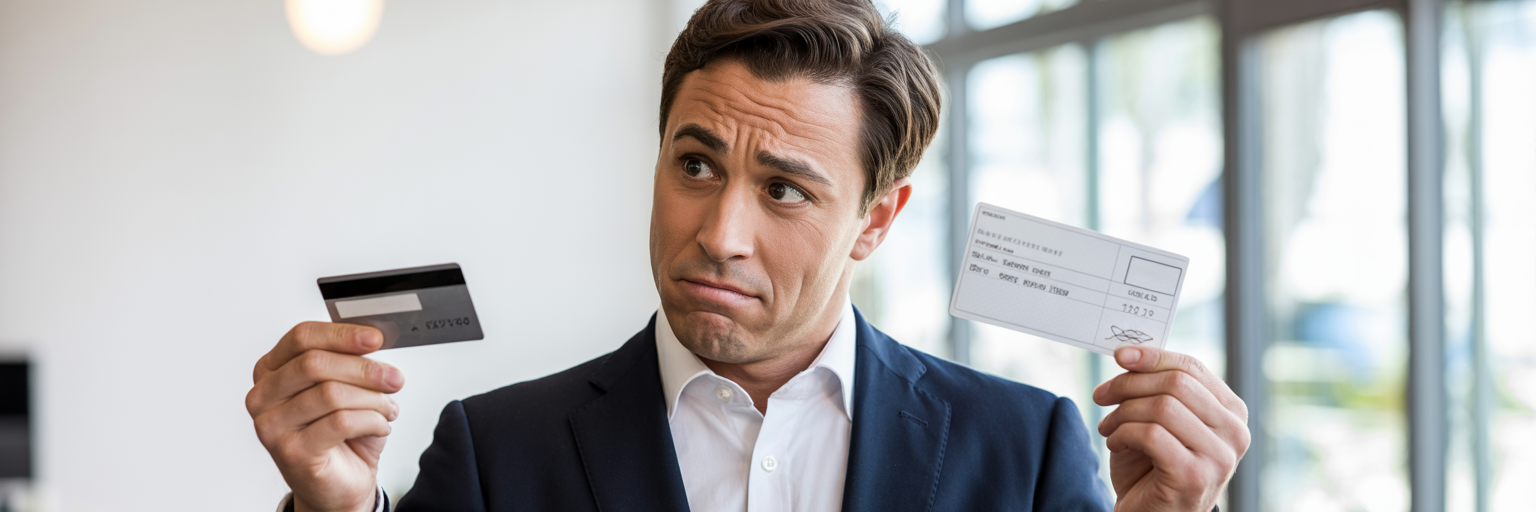

Paycards and direct deposit for employees are both popular employee payment options in the modern world.

Paycards and direct deposit for employees are both popular employee payment options in the modern world.

Direct deposit sends wages directly to a worker’s bank account, while paycards load pay onto a card that can be used like a debit card.

They both have obvious benefits and drawbacks for the employee and employer. To assist owners and managers in choosing the best option, this guide will break down the highlights and important information about both.

Key Takeaways

- Paycards provide instant access to wages and can be a smart choice for unbanked employees, supporting financial inclusion in a multicultural workforce.

- Direct deposit is fast, inexpensive, and promotes financial wellness for banked employees by facilitating automatic transfers to savings and ensuring dependable wage delivery.

- Tech-savvy employees worldwide may benefit as digital wallets and new payroll technologies speed up, secure, and expand access to wage payments.

- It reinforced the importance of fee transparency, legal compliance, and clear communication for employers and employees alike when selecting or implementing paycard or direct deposit programs.

- As discussed, employers need to consider employee preferences, demographics, and financial literacy when determining whether paycards or direct deposit is best to ensure increased retention and satisfaction.

- By keeping up with new regulations and payment technologies, they keep their organizations compliant and competitive in a global workforce.

Is Your Payroll Pay Card Program Compliant?

Offering payroll pay cards across multiple states is not simply an operational decision — it is a legal compliance decision.

Each state has different wage payment rules, consent requirements, and fee restrictions. A program that is compliant in one jurisdiction may create liability in another.

Before implementing or expanding a payroll pay card program, ask:

-

Are you obtaining legally sufficient written consent?

-

Can employees access 100% of net wages without fees?

-

Are vendor fees creating unlawful wage deductions?

-

Are your disclosures compliant with federal EFTA requirements?

-

Have you reviewed the wage payment statute in each state where you operate?

Failure in any one of these areas can expose your organization to:

-

Wage claims

-

Regulatory investigations

-

Class action litigation

-

Civil penalties

-

Reputational harm

Payroll Compliance Should Be Strategic — Not Reactive

At My Virtual HR Director, we help employers:

-

Evaluate multi-state payroll compliance risks

-

Audit payroll pay card programs

-

Implement legally compliant wage payment systems

-

Reduce exposure to payroll-related litigation

-

Strengthen internal payroll controls

Whether you operate in one state or all fifty, we help you structure payroll systems that align with both operational efficiency and regulatory protection.

👉 Review Your Payroll Risk Exposure Today

If you are currently using — or considering using — payroll pay cards, schedule a compliance review before rollout.

Protect your organization. Protect your employees. Protect your payroll system.

What are Paycards and Direct Deposit?

Paycards and direct deposit are two of the most popular methods of paying employees in the modern workplace. Both eliminate the paper check and streamline payroll for employers and employees alike.

Paycards function as prepaid debit cards, enabling employees to spend wages up to their balance, pay bills, make purchases, or obtain ATM cash withdrawals. These cards are not linked to the employee’s personal bank account but rather are handled by a third-party provider.

Direct deposit means the employer electronically sends wages directly into an employee’s bank account. More than 95% of employees are paid this way today, showing how common it has become. Both are popular with businesses that want to keep payroll simple, fast, and reliable.

With digital payment options increasing, some companies are seeking to serve workers who might shun traditional banks, so paycards can be a compelling alternative.

The Digital Wallet

A digital wallet is an app or software that stores payment details securely on a phone or computer. It enables users to pay or be paid without a physical card.

For instance, a worker can swipe from their digital wallet to immediately cover lunch or send money to a peer. Paired with payroll, digital wallets enable frictionless payments. Wages can flow directly from the employer into the worker’s digital wallet, available immediately.

It’s especially nice for workers who crave immediacy and choice in payments. Digital wallets are catching on with early adopters who appreciate convenience and security. A few companies even allow employees to have their pay deposited directly to a digital wallet, bypassing the bank account or even the paycard.

The Bank Transfer

Direct deposit depends on bank transfers to send funds from employer to employee. The employer’s payroll system sends wage information to his bank, which pushes funds electronically to each employee’s account.

It cuts payroll processing time and errors versus checks. The security of these transfers relies on longstanding banking networks that most people already trust. Such a system only works if the employee’s bank information is accurate—errors can cause pay to be late or missing.

For a lot of companies, the speed and ubiquity of bank transfers means direct deposit is their payroll method of choice. Not all employees have bank accounts, so providing paycards as an option is often mandated and everyone can get paid on time.

Paycards vs Direct Deposit for Employees

Employee wage payment options have evolved rapidly in recent years. While the majority still use direct deposit payments, paycards are rapidly emerging as a viable alternative for businesses. Each payment option works differently and suits different needs, especially for unbanked employees. For employers — particularly those with diverse teams — it’s important to understand how paycard benefits impact access, cost, security, and convenience, as well as the financial impact on workers.

1. Access

Paycards provide immediate access to wages on payday, a critical feature for unbanked workers. With nearly a quarter of American households unbanked or underbanked, this is not a fringe concept either. Paycards work at ATMs and can be used for purchases just like debit cards, so employees don’t have to wait for checks to clear or make trips to the bank.

Direct deposit requires a bank account. Although it’s easy for the majority, it excludes workers who either don’t want or can’t have a traditional bank account. For a paycheck-to-paycheck worker, having immediate access to their earnings can be the difference in paying rent, putting food on the table, or addressing that emergency.

2. Costs

Paycards can have various fees such as ATMs, balance inquiry, and monthly maintenance. These fees can devour wages if you’re not vigilant. Direct deposit is typically free to employees and is considered the least expensive payment method.

For the business, direct deposit can save money by eliminating paper checks and minimizing payroll mistakes. Paycards could cost less than a check, but the fees need to be transparent. No employee should be shocked by lost wages due to hidden fees.

3. Security

Paycards have PIN codes and fraud alerts and are therefore safer than paper checks. They can be lost or stolen. Direct deposit utilizes bank-level security, with funds transferred directly into an account, so it is less susceptible to theft.

If a paycard is lost, it is replaceable; however, there may be a delay in recovering funds. Whether employees receive paycard or bank details, they should know how to protect them.

4. Convenience

Paycards are nice for employees who want cashless pay but don’t want a bank account. They can be reloaded and used pretty much anywhere. Direct deposit is simple to arrange via payroll and demands minimal maintenance.

For workers who prefer their pay deposited into multiple accounts, such as a savings or retirement account, direct deposit enables automatic splits. The optimal choice is what best suits a worker’s lifestyle and financial habits.

- Direct deposit typically posts funds by midnight or the next business day.

- Paycards can be immediate on payday, but there is occasionally a brief processing delay.

- Bank holidays can bog down both methods, although direct deposit typically catches up after a few days.

- Paycard access can be disrupted if the card is lost or damaged.

5. Financial Impact

Paycards assist unbanked employees manage money without resorting to check-cashing stores. They simplify budgeting since paychecks are all set to spend or pull out. Direct deposit encourages savings by allowing employees to divide deposits.

Both can boost money skills with the right tools. If your company gives employees choice, they feel appreciated and stick around. Paycards vs direct deposit for employees.

The Employer's Choice

Employers have to consider every factor when choosing between paycards and direct deposit. It’s not just choosing a payroll system—it’s a juggling act between cost, compliance, and employee wellbeing. Direct deposit is still the norm in the US, with more than 95% of workers paid this way.

Paycards can fill a gap, particularly for unbanked or underbanked employees. The employer’s choice, done right, can increase satisfaction and aid in recruiting and retention, particularly when employers offer a variety of options. Employees want flexibility, and they want holistic benefits.

About 80% say that they want benefits that support their financial health. Providing both paycards and direct deposit gives employees options and can lower attrition, particularly if you include perks such as early wage access, which has been proven to boost employee morale and loyalty to the company.

PRO TIP:

It is not legal in all fifty states to offer pay cards. See our compliance section of this stroy below to check if your state allows it. It is also important to note that even when it is allowed and legal, many states do not allow employers to force employees to receive direct deposit or to receive a pay card. Even if you do cxhoose to offer direct deposit and/or pay cards, be sure to abide by all notice and release requirements of your state.Implementation

Implementing a paycard program requires smart strategy and defined stages. Here’s how I’ve seen it work best:

-

Select a trusted paycard partner with payroll compliance experience.

-

Consult both local and federal regulations to ensure you provide alternative forms of payment such as direct deposit or paper checks.

-

Arrange the technology to connect your payroll system with the paycard provider.

-

Train HR and payroll staff on the new process.

-

Be upfront with employees and educate them on the paycard option, how it functions, and any potential fees.

-

Allow employees time to inquire and select the payment method that is convenient for them.

Sometimes employers get pushback from employees who are skeptical of new technology or fees. I’ve witnessed success when employers provide side-by-side comparisons and conduct small pilot groups prior to a complete launch.

Administration

Administering paycards is a continuous concern. Payroll teams have to keep tabs on payments, lost cards, and issues like card freezes, which can occur with certain hotels or rental car companies. You should maintain current records for each employee’s pay, independent of the process.

Payroll providers can automate payments and flag compliance risks, taking much of the burden off HR. Even with good vendors, employers have to maintain a regular audit of records and procedures to trap mistakes. Consistency and accuracy are key here.

Compliance

Legal compliance is a given. Employers must always provide an alternative to paycards, typically direct deposit or paper check, so employees aren’t forced into a single option. It’s imperative to comply with every wage payment statute on the state and federal level, which includes providing transparent disclosures of any fees or conditions associated with paycards.

Non-compliance can mean expensive legal fines and a tarnished reputation. It’s always best to run each step by legal counsel and ensure your payment choices are equitable and fully transparent.

Check out the full compliance-by-state section of this article. (Not legal or tax advice.)The Employee's Reality

For employees, paycards and direct deposit are almost never one-size-fits-all. Real paystub problems tend to come down to who owns a bank, who doesn’t, and the stress employees experience each pay cycle. Financial stress is the norm. Nearly 80% of US full-time workers live paycheck to paycheck, and just a week’s delay in pay would leave more than 78% struggling.

This story unfolds differently for the banked and unbanked, for whom payroll decisions influence not only day-to-day life but retention and morale.

The Banked

Direct deposit is par for the course for most employees with a bank account. More than 95% of working people get paid like this. For these workers, direct deposit isn’t just a convenience; it’s a path toward feeling financially stable and confident. They don’t stress about dropping a check or standing in line at the check-cashing joint. Their cash comes in on the schedule every time, thanks to popular paperless payment methods like pay cards.

Direct deposit merely reduces the friction for the banked to manage their money. It secures their pay, reduces downtime, and connects directly to digital platforms for budgeting or bill pay, enhancing the overall payroll options available.

- No need to visit a bank or cash check

- Easier to track pay and savings

- Faster access to funds

- Less risk of theft or loss

- Streamlined bill payments and transfers

Direct deposit fosters confidence in payroll. When pay lands in accounts on time, every time, employees experience dependability. This dependability may increase loyalty and create stickiness among employees, especially for those using electronic payment methods.

In my decades working behind the scenes for tens of thousands of companies, I noticed retention increase when pay was instant and frictionless for miles of employees. The reassurance is tangible.

The Unbanked

Workers with no bank account have it even worse. Approximately eight point four million US households are unbanked and 24.2 million are underbanked. A lot of these workers are already on the edge financially, unable to afford a $400 emergency and paying overdraft fees for necessities.

Barriers such as credit history, minimum balance policies, and expensive fees put banking out of reach for many, particularly African American and Latino American communities.

Paycards are an effective solution in this place. They act like a debit card and permit unbanked workers to receive their earnings electronically, shop online, pay bills, and take out cash at ATMs. Not even a bank account is needed.

When you provide paycards to small business owners, it translates to better retention, less late payroll stress, and a more inclusive office. When employees know they have choices, morale rises.

Paycards provide a bridge. Distributing cards alone is insufficient. A lot of unbanked employees require assistance with fees, digital tools or financial planning. Education is critical.

It demonstrates how paycards function, locations with the lowest fees, and how to utilize benefits such as early wage access. Supported employees stick around, and research reveals that early access to wages earned increases morale and retention.

Are Payroll Paycards Legal?

Payroll paycards are an increasingly common method of paying employees in many jurisdictions. They act like debit cards, preloaded with every paycheck. They’re legal in large parts of the US and lawful as a form of wage payment. In 28 states, laws or regulations explicitly enumerate paycards as permitted.

In many other states, wage and hour offices accept them as a valid form of payment, even if not listed in their statutes. This is key for businesses with employees in multiple states. Certain states, such as Oklahoma and West Virginia, recently amended their laws to establish clearer regulations for paycards.

Employers have a laundry list of regulations to observe when they utilize paycards. These regulations are at both the federal and state level. At the federal level, the CFPB sets rules for any prepaid account, including paycards. The primary law is the EFT Act and Regulation E.

This law governs how employees receive their wages and defines the rights of the employee. The law says workers must have a choice regarding how they receive their pay. No one can make paycards mandatory for workers. Consumers need to be able to access all their pay in cash with no sneaky fees or tricks.

They state employees must receive a complete fee schedule, and the card must be user-friendly. If a card is lost or stolen, the law limits the worker’s loss if they act quickly. All employers should know that every state has its own spin on paycard regulations.

Certain states, including New York, New Jersey, and Illinois, are very restrictive on written consent and fee limits. Others are floppier. If a company uses paycards in multiple states, it must verify the regulations in each jurisdiction. Not complying can mean big fines, lawsuits, or claims for unpaid wages.

I just saw a client company in the hospitality industry get hit with a big penalty when they missed a new state rule on paycard fees. The danger is tangible, and it’s not merely a regulatory dictate. In certain industries, a large proportion of employees are unbanked or underbanked.

For them, paycards are a life-changer, allowing them to circumvent check-cashing stores and get their money more quickly. It only works great if the company establishes the program correctly and complies with the legislation.

*Compliance By State:

New Jersey Employer? Here Are Your Requirements for Paying Employees with a Pay Card:

Are Paycards permitted under New Jersey Law?

Pay cards are permitted under New Jersey law — but they are heavily regulated. If your organization is considering offering pay cards as a wage payment option, compliance with the New Jersey Wage Payment Law and N.J.A.C. 12:55-2.4 is mandatory. Below is what employers must do to remain compliant.

1. Obtain Voluntary Written Consent

New Jersey employers cannot require employees to accept wages via pay card.

Before using a pay card, you must:

-

Obtain written authorization from the employee

-

Ensure consent is given voluntarily, without intimidation or coercion

-

Confirm that accepting a pay card is not a condition of hire or continued employment

-

Allow the employee to withdraw consent at any time

If an employee declines, you must provide another lawful payment method, such as paper check or direct deposit.

2. Provide Clear Written Disclosures

Prior to enrollment, employers must provide written disclosures explaining:

-

How the pay card works

-

How wages are deposited

-

All potential fees associated with the card

-

How employees can access their full wages

-

How to obtain transaction histories

-

How to opt out

These disclosures must be transparent and understandable. Failure to properly disclose fee structures is a common compliance violation.

3. Ensure Access to 100% of Net Wages — Without Fees

This is one of the most critical legal requirements.

Employees must be able to:

-

Access their full net wages

-

At least once per pay period

-

Without incurring any fee

If ATM withdrawal limits, point-of-sale restrictions, or transaction fees prevent employees from accessing their entire paycheck without cost, the pay card arrangement may violate New Jersey law.

4. Avoid Impermissible Fees or Wage Deductions

Employers cannot shift payroll costs onto employees.

A pay card program may create liability if:

-

Fees reduce wages below minimum wage

-

Routine transactions generate unavoidable charges

-

Fees operate as de facto wage deductions

Employers are responsible for vetting their pay card vendor and monitoring the fee structure to ensure ongoing compliance.

5. Maintain All Standard Wage Payment Protections

Using pay cards does not change any other wage payment obligations. Employers must still comply with:

-

Regular pay frequency requirements

-

Overtime payment laws

-

Final paycheck timing rules

-

Wage statement requirements

A pay card is simply a delivery mechanism — it does not modify underlying wage laws.

6. Allow Employees to Opt Out

Employees must have the ability to discontinue pay card participation and choose another lawful payment method. Employers cannot “lock” employees into the program.

Compliance Wrap Up: Risk Considerations for Employers

While pay cards can provide flexibility for unbanked employees, they introduce additional compliance risks, including:

-

Documentation and consent tracking exposure

-

Fee structure scrutiny

-

Vendor oversight obligations

-

Potential wage deduction claims

-

Class action risk for systemic violations

For many employers, careful implementation and internal controls are essential before rolling out a pay card program.

If you choose to offer payroll pay cards in New Jersey, strict adherence to these requirements is not optional — it is the difference between a compliant payroll system and a costly wage claim.

The Future of Employee Pay

Employee pay is evolving rapidly, influenced by emerging technologies, employee demands, and global forces. Digital payments are replacing old paper checks, making payroll simple, fast, and flexible. Employers across the board now realize that cookie-cutter pay doesn’t cut it for a varied, worldwide employee base. Options such as direct deposit, payroll cards, and even early wage access are going from nice to have to need to have.

Digital payroll solutions are thriving. Almost all workers, particularly younger ones, favor contactless and digital pay. Research indicates that 85% of Gen Z and 82% of Millennials prefer digital pay options. This crew anticipates quick, convenient, and secure compensation. During my tenure in HR, I’ve witnessed disgruntled employees jump ship simply because a business couldn’t provide direct deposit or a paycard.

Waiting for paper checks to come slows down people’s lives. For employers, it costs between $2 and $4 to cut a single check. Multiplying that by hundreds of checks accumulates costs quickly. Digital payments, especially through payroll debit card accounts, cut these costs and liberate resources.

New tech is making it even sleeker. Banks and financial firms are investing serious cash in better payment tech. Ninety-four percent of banks are currently spending on new systems. Paycards and electronic payment tools are transforming payroll. These choices allow employees to receive their wages immediately or even access a portion of their wages ahead of time.

I’ve witnessed morale soar when firms provide early access to pay. Employees are less stressed, stick around longer, and feel that their employer cares about them. For employees scraping by, this could be a lifeline.

Employers can’t overlook the unbanked or underbanked individuals, either. Close to one-fourth of US households are unbanked or underbanked, and globally, the situation is worse. Paycards allow these workers to receive compensation without a traditional bank account. I worked with a healthcare client who switched to paycards, and we saw both lower turnover and fewer payroll headaches.

Seventy-eight percent of employees say a missed or late paycheck would make it difficult to pay bills. Providing additional pay choices fosters trust and retains teams.

Payroll rules and employee rights keep changing. Pay transparency is gaining momentum, with additional states requiring companies to provide pay data and allow employees to discuss wages. Employers need to be on top of these shifts or face fines or lawsuits.

Be open and flexible with pay; it builds loyalty and keeps companies ahead of the curve.

Your Bottom Line

Paycards vs direct deposit employees both deliver pay to workers quickly. Some prefer cards for instant spending and zero bank visits. Others want pay in their own bank and more control. Laws keep changing, so bosses had better check rules in their location. Few stores pocket savings with paycards versus direct deposit employees. Other employees think cards assist those without banks. Both sides deserve straightforward information. At My Virtual HR Director, we assist organizations choose what’s right. We’ve aided shops with five employees and large corporations as well. Want to get pay right for your shop? Call us. We believe pay should be simple, fair, and fast for everyone. Let’s discuss what makes sense for your crew.

Frequently Asked Questions

What is the main difference between paycards and direct deposit?

Paycards are prepaid cards with wages loaded on them, providing a flexible pay option for unbanked employees. Direct deposit delivers funds straight to an employee’s account, but paycard benefits include accessibility without needing traditional bank accounts.

Are paycards safe for employees to use?

Yes, paycards are safe and offer significant paycard benefits. Most come with loss and theft protections, similar to traditional bank accounts.

Can employees choose between paycards and direct deposit?

In most places, employees can decide between payroll options. Employers ought to provide both payment methods where feasible, including pay cards and direct deposit arrangements.

Do paycards have fees?

Most paycards, a popular paperless payment method, charge fees for certain transactions, like ATM withdrawals or balance inquiries, so workers must check all paycard fees before using a paycard.

Is direct deposit faster than paycards?

Both direct deposit payments and paycards are convenient and timely payroll options, with direct deposit frequently arriving on payday and paycards allowing for fast access to funds.

Are payroll paycards legal worldwide?

It depends on the countries' laws regarding payroll cards. In certain regions, paycards are prevalent and overseen, while in others, they might even have limitations. Employers need to check with local labor laws.

What is the future of employee pay methods?

Digital payments, including popular paperless payment methods like paycards, are going to grow globally. A growing number of employers provide multiple flexible payroll options such as instant payments to accommodate employees’ different needs.

Joseph Campagna, SPHR, SHRM-SCP is president and owner of My Virtual HR Director, a human resources outsourcing company serving small and medium sized businesses nationwide. My Virtual HR Director provides an executive level HR advisor to companies that can’t afford or can’t justify hiring a fulltime HR professional on staff.

With thirty years of experience dedicated to the HR profession, Mr. Campagna has honed his skills as an expert in compliance, talent management and employee relations. Bringing human capital management experience from start-ups, IT and biotechnology companies, employee leasing, and fortune 100 behemoths Mr. Campagna has filled his tool belt through generalist work, executive positions, and consulting opportunities with companies such as ADP, Merrill Lynch, and Johnson & Johnson. As Vice President of HR for biotech company Hemo Concepts, as well as the head of HR for the global IT solutions company, the Galaxy Group, Mr. Campagna created rich and successful organizational development and employee engagement programs.

Having worked with a diverse group of companies and clients in a broad spectrum of industries and environments, he brings a unique HR philosophy to every organization he works with. “HR is not the picnic department,” he says “but instead bears the full responsibility and the unlimited potential for a highly productive and efficient workforce. If HR systems are successful, the organization’s revenue should be increased.” From mergers and acquisitions, to IPO’s, to new product development, to divestiture Mr. Campagna has a true business background to support his HR Architecture.

Mr. Campagna is certified as a senior professional through both the Human Resources Certification Institute (HRCI) and the Society for Human Resource Management (SHRM). The HRCI designation of Senior Professional in Human Resources (SPHR) is an experienced-based examination certification. The SHRM certification is a competency based examination certification. Each is a premier designation in the world of HR and recognized by the Society for Human Resource Management of which Joe is a national member and former chapter president.

Mr. Campagna brings decades of helping small and medium sized businesses create HR structures such as employee handbooks, performance systems, talent management, training programs, and employee engagement. He knows how to deliver business results through HR aligned objectives.

Nearly 30 years of expertise and HR executive authority combined with a group health insurance license and certifications from the Society for Human Resource management and the Human Resources Certification Institute have given Joseph Campagna the guru status that has earned him leadership roles, board of director roles, and speaking engagements related to human resources.